All Categories

Featured

Table of Contents

If George is detected with a terminal disease throughout the initial policy term, he probably will not be qualified to restore the plan when it ends. Some policies offer ensured re-insurability (without proof of insurability), however such features come at a greater cost. There are a number of sorts of term life insurance policy.

Typically, most companies provide terms ranging from 10 to 30 years, although a couple of deal 35- and 40-year terms. Level-premium insurance policy has a set monthly settlement for the life of the policy. Most term life insurance policy has a level costs, and it's the type we have actually been referring to in a lot of this post.

Term life insurance policy is appealing to young individuals with youngsters. Parents can obtain considerable coverage for an inexpensive, and if the insured passes away while the plan is in result, the family members can rely upon the fatality advantage to change lost income. These plans are likewise fit for individuals with growing households.

What is Level Premium Term Life Insurance? Learn the Basics?

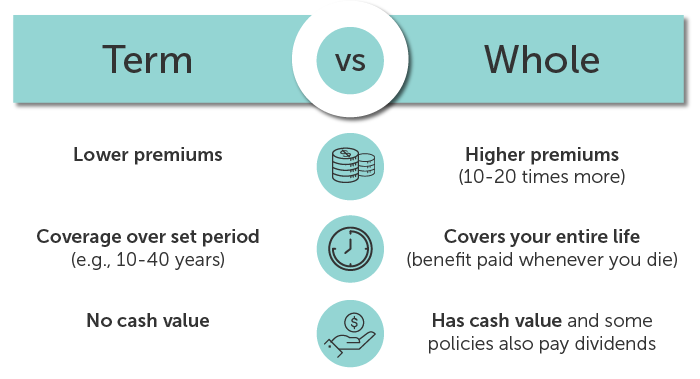

Term life policies are optimal for people that desire significant coverage at a low price. People who have whole life insurance coverage pay more in costs for much less coverage however have the safety and security of recognizing they are safeguarded for life.

The conversion biker should permit you to convert to any kind of irreversible plan the insurance provider uses without restrictions. The key features of the rider are keeping the initial health ranking of the term plan upon conversion (also if you later have wellness concerns or end up being uninsurable) and making a decision when and just how much of the protection to transform.

Of course, general premiums will certainly raise substantially considering that whole life insurance policy is more costly than term life insurance coverage. The advantage is the guaranteed approval without a medical examination. Medical conditions that establish during the term life duration can not create costs to be boosted. However, the firm may require restricted or full underwriting if you wish to include added bikers to the new plan, such as a long-term care cyclist.

What Makes 20-year Level Term Life Insurance Different?

Term life insurance policy is a relatively affordable method to offer a lump amount to your dependents if something happens to you. It can be an excellent option if you are young and healthy and balanced and support a family. Whole life insurance policy comes with substantially higher month-to-month costs. It is suggested to give coverage for as lengthy as you live.

It depends on their age. Insurance business established a maximum age limit for term life insurance policy policies. This is typically 80 to 90 years of ages yet might be higher or reduced relying on the firm. The premium also climbs with age, so an individual matured 60 or 70 will certainly pay considerably more than a person decades younger.

Term life is somewhat similar to cars and truck insurance coverage. It's statistically not likely that you'll require it, and the premiums are money away if you don't. If the worst takes place, your family members will obtain the benefits.

How Does Term Life Insurance For Couples Work for Families?

Essentially, there are 2 kinds of life insurance coverage plans - either term or long-term plans or some mix of the 2. Life insurance firms use different types of term plans and standard life plans in addition to "interest delicate" items which have actually come to be a lot more widespread because the 1980's.

Term insurance offers defense for a given time period. This duration could be as short as one year or offer coverage for a specific variety of years such as 5, 10, 20 years or to a defined age such as 80 or in many cases approximately the earliest age in the life insurance policy death tables.

What is the Role of Term Life Insurance?

Presently term insurance policy rates are extremely affordable and among the most affordable historically experienced. It should be noted that it is an extensively held idea that term insurance is the least expensive pure life insurance protection offered. One requires to review the plan terms carefully to choose which term life alternatives are ideal to meet your certain circumstances.

With each brand-new term the premium is enhanced. The right to renew the plan without proof of insurability is a crucial advantage to you. Otherwise, the threat you take is that your wellness may wear away and you may be incapable to acquire a plan at the very same rates and even in all, leaving you and your recipients without coverage.

You need to exercise this choice throughout the conversion duration. The size of the conversion duration will certainly differ depending on the sort of term policy acquired. If you convert within the proposed duration, you are not required to give any details about your wellness. The premium price you pay on conversion is normally based on your "existing achieved age", which is your age on the conversion day.

Under a level term policy the face quantity of the plan continues to be the exact same for the whole duration. Frequently such policies are offered as home loan protection with the amount of insurance coverage decreasing as the equilibrium of the home loan reduces.

Traditionally, insurers have not can change costs after the policy is offered. Because such plans may proceed for several years, insurance providers should make use of conservative mortality, passion and expense price estimates in the premium calculation. Adjustable costs insurance policy, nevertheless, allows insurance companies to offer insurance at lower "existing" premiums based upon much less traditional presumptions with the right to transform these costs in the future.

How Does Level Term Life Insurance Policy Keep You Protected?

While term insurance is developed to provide defense for a specified time period, long-term insurance is developed to supply protection for your whole life time. To keep the premium rate level, the premium at the more youthful ages surpasses the actual expense of defense. This added costs develops a reserve (money value) which aids spend for the plan in later years as the price of protection surges above the costs.

Under some policies, costs are required to be spent for a set number of years (Term life insurance for couples). Under various other policies, costs are paid throughout the policyholder's lifetime. The insurance provider spends the excess premium dollars This type of policy, which is sometimes called cash money value life insurance coverage, produces a financial savings component. Cash worths are crucial to an irreversible life insurance policy plan.

Sometimes, there is no correlation in between the size of the cash worth and the premiums paid. It is the cash value of the policy that can be accessed while the insurance holder is active. The Commissioners 1980 Requirement Ordinary Mortality (CSO) is the present table utilized in computing minimum nonforfeiture worths and plan gets for common life insurance policy plans.

What is What Is Direct Term Life Insurance? What You Need to Know?

Lots of long-term plans will certainly have stipulations, which specify these tax needs. There are 2 standard groups of long-term insurance, typical and interest-sensitive, each with a number of variants. Furthermore, each category is generally available in either fixed-dollar or variable form. Traditional entire life plans are based upon lasting estimates of expenditure, rate of interest and mortality.

{kind=link}

Latest Posts

New Funeral Expense Benefit

Funeral Expenses Plan

Best Burial